When Will the Fed Start Cutting Interest Rates?

Our latest economic forecast for interest rates, inflation, and GDP growth.

Wondering what’s in store for interest rates?

Although the Federal Reserve continues its campaign of hiking interest rates—and economic turbulence persists—our long-term optimism about gross domestic product and inflation remains largely unchanged.

In our latest Economic Outlook, we detail that although a recession in the next 12 months remains a serious possibility (about a 30% to 40% chance), it should be short-lived if it occurs. Once the Fed wins the war against inflation, it will shift to cutting interest rates in order to get the economy moving again.

Why Have Interest Rates Increased So Much in 2022 and 2023?

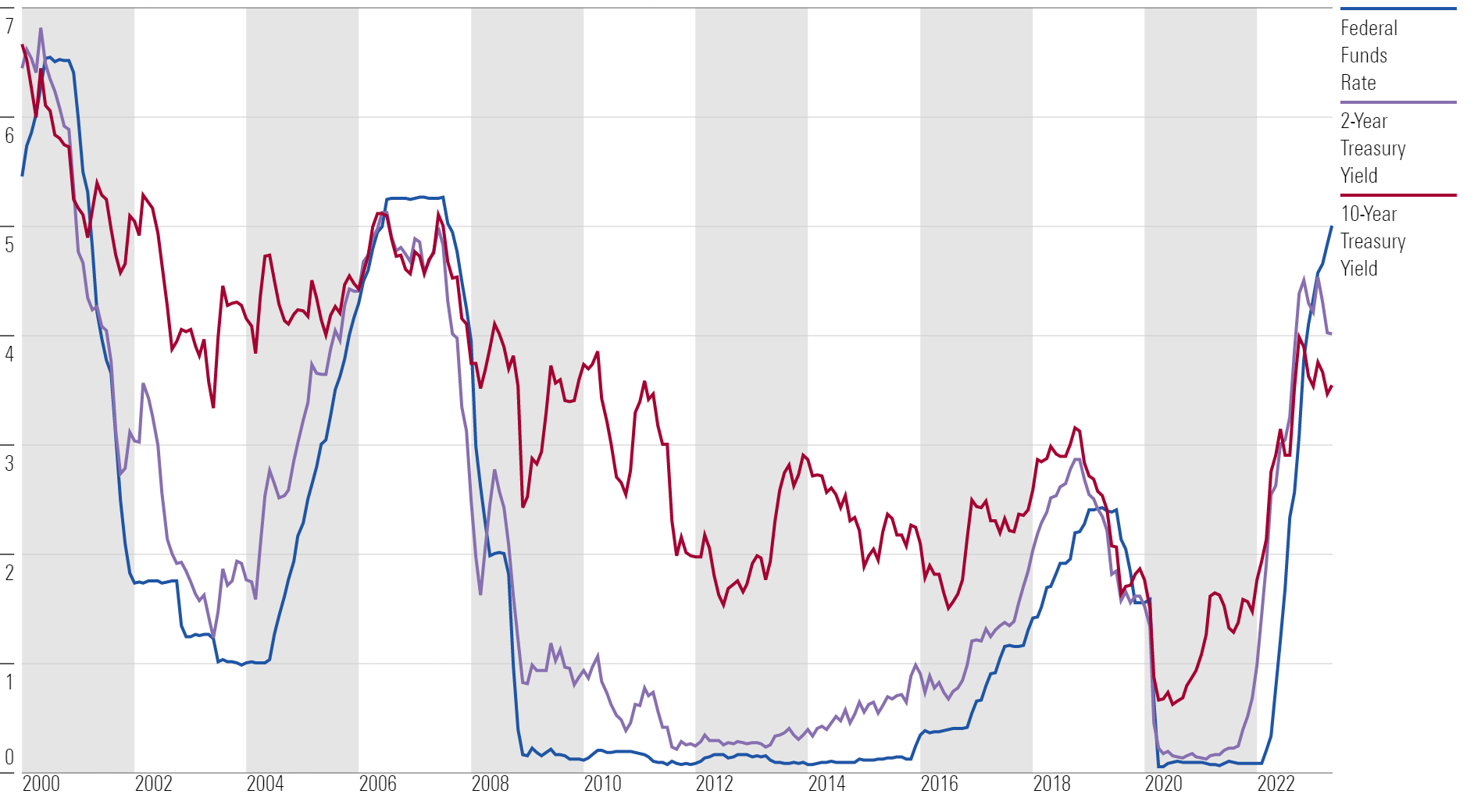

The Fed has pushed interest rates higher for more than a year in order to quash high inflation. It’s done this by hiking the federal-funds rate and other measures, which has driven interest rates to levels not seen since the late 2000s, before the global financial crisis.

The United States (and many other countries) had experienced a decade of low interest rates after the 2008 crisis and the Great Recession, but many investors are now wondering whether that era has ended for good.

U.S. Interest Rates

Higher interest rates have meant higher borrowing costs for consumers and businesses. The 30-year mortgage rate reached 7% at one point in November 2022, the highest in over 20 years. This is causing a slowdown in spending in housing and other sectors of the economy. This is by design—the Fed must rein in spending in order to bring inflation down.

One reason that interest rates have risen much further than most forecasters (including us) anticipated is that the U.S. economy has proved more resilient to the impact of higher rates than expected. Housing activity has fallen sharply, but much of the rest of the economy seems unscathed. We think that households’ excess savings and other factors are temporarily cushioning the hit from higher interest rates. Over the coming year, we expect the impact of rate hikes to be felt more strongly in other parts of the U.S. economy.

When Will Interest Rates Go Down?

First, we expect the Fed to pause its rate hikes by summer 2023 (the May hike was the last one, in our view). Then, starting around the end of 2023, we expect the Fed to begin cutting the federal-funds rate.

The Fed will pivot to monetary easing as inflation falls back to its 2% target and the need to shore up economic growth becomes a top concern.

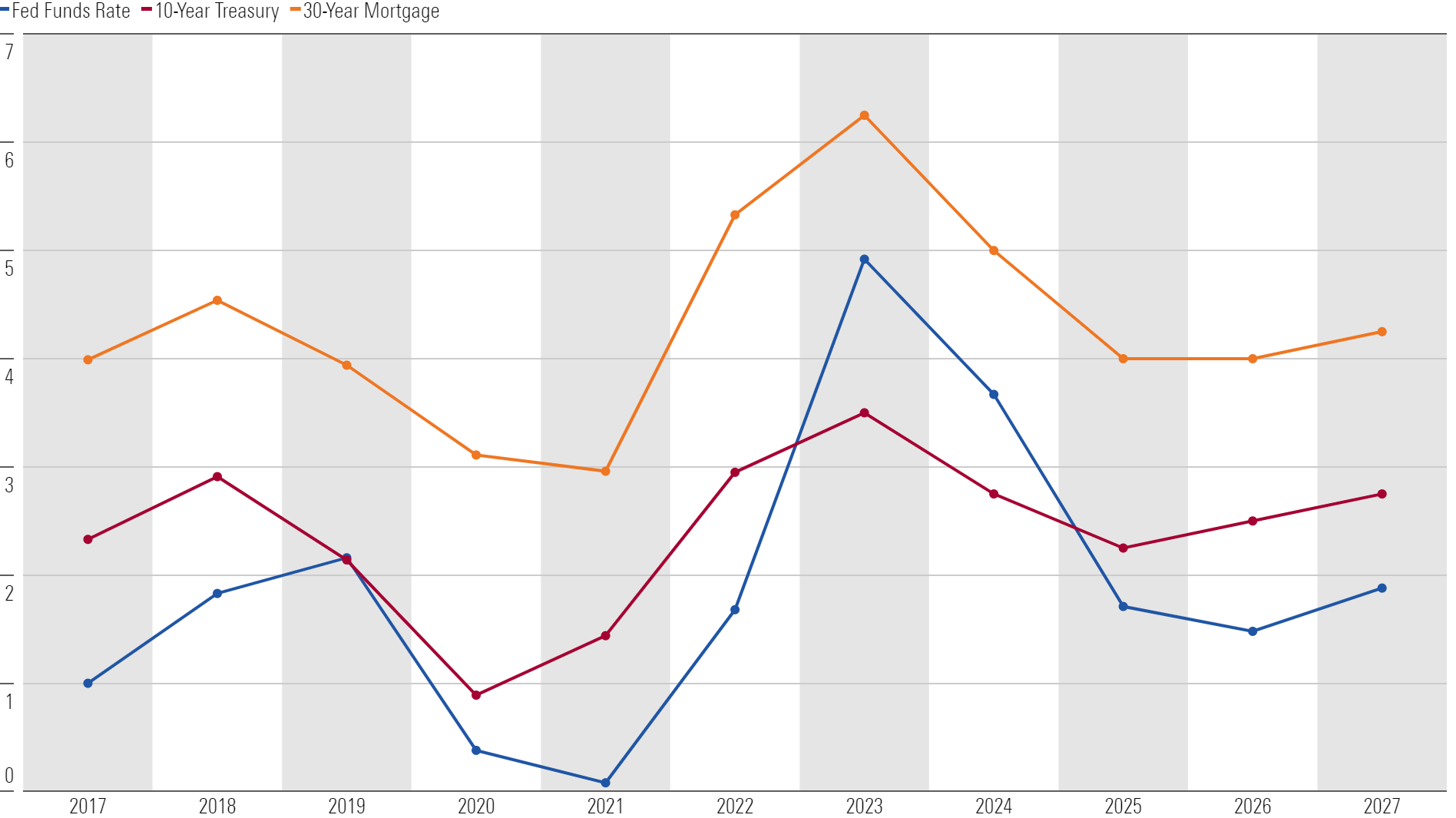

1) Interest-rate forecast. We project a year-end 2023 federal-funds rate of 4.75%, falling below 2.00% by mid-2025. That will help drive the 10-year Treasury yield down to 2.25% in 2025 from an average of 3.5% in 2023. We expect the 30-year mortgage rate to fall from an average 6.25% in 2025 to 4% in 2025.

2) Inflation forecast. We project price pressures to swing from inflationary to deflationary in 2023 and following years, owing greatly to the unwinding of price spikes caused by supply constraints in durables, energy, and other areas. This will make the Fed’s job of curtailing inflation much easier. In fact, we think the Fed will overshoot its goal, with inflation averaging 1.8% over 2024-27.

The inflation analysis is critical to our near-term projections for GDP and interest rates. If inflation becomes much more entrenched, the Fed will have to engineer a sharp short-run recession by hiking interest rates much higher than we expect.

Interest Rate Forecasts (Annual Avg)

As long as the Fed is allowed to shift to easing by the end of 2023, GDP should avoid a large downturn and start to accelerate in 2024 and 2025. Housing, which is the most interest-rate-sensitive major component of the GDP, will drive much of the fluctuation in GDP growth. Lower rates in 2024 and 2025 will be needed to improve housing affordability via lower mortgage rates and thereby resuscitate demand in an ailing housing market.

For investors, the Fed’s pivot should provide welcome relief. Rising interest rates played a key role in the selloff in both stocks and bonds in 2022. Bonds will certainly rally if yields fall in line with our forecasts for the next five years. And while not guaranteed, we expect that falling interest rates would likely also lift stock prices. Borrowers will also see relief as rates come down; 2025 should be a good time to refinance for those who took out a home mortgage at elevated rates.

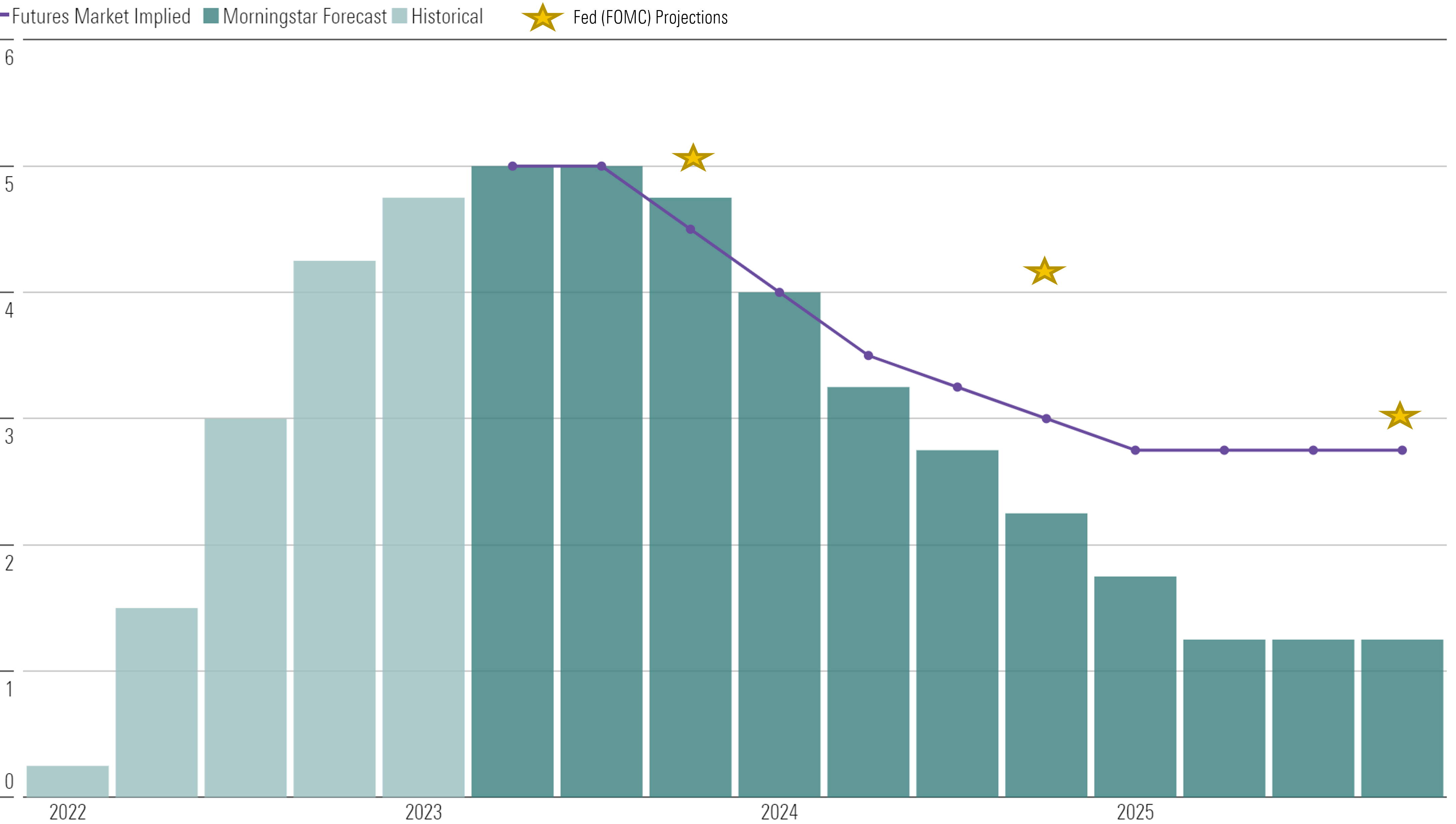

Why Do We Disagree With Other Investors (and the Fed) on How Quickly Interest Rates Will Fall?

Our expected path for the federal-funds rate is below what other investors are expecting, as gauged by the federal-funds futures market. The Fed’s own projections are even further above the market expectations. The difference starts small, but by the end of 2024, we expect a federal-funds rate around 1 percentage point below the market’s projection and 2 percentage points below the Fed’s.

Fed-Funds Rate (%) Expectations (Bottom of Target Range)

Why do we think we know what the Fed will do better than the Fed itself? Ultimately, the Fed will adjust to the incoming data. At many points in the past 10 years (when the Fed first started issuing multiyear projections for the federal-funds rate), the Fed has veered from its initial forecasts owing to shifts in the data.

We expect inflation to come down quicker than the Fed expects, which is why we expect the Fed to eventually cut interest rates more aggressively than it currently projects. Likewise, other investors now appear too pessimistic on how quickly inflation will fall.

What about the recent spate of financial distress, including two high-profile bank failures? We’ve argued that recent events are not a game changer for monetary policy. The Fed is going to use liquidity injections to keep distress under control, while continuing to keep the federal-funds rate restrictive in 2023 in order to fight inflation. So far this is playing out, and deposit outflows from banks have been muted recently after massive outflows in early March. In our view, this financial-sector fragility isn’t anywhere near as bad as the runup to the 2008 crisis.

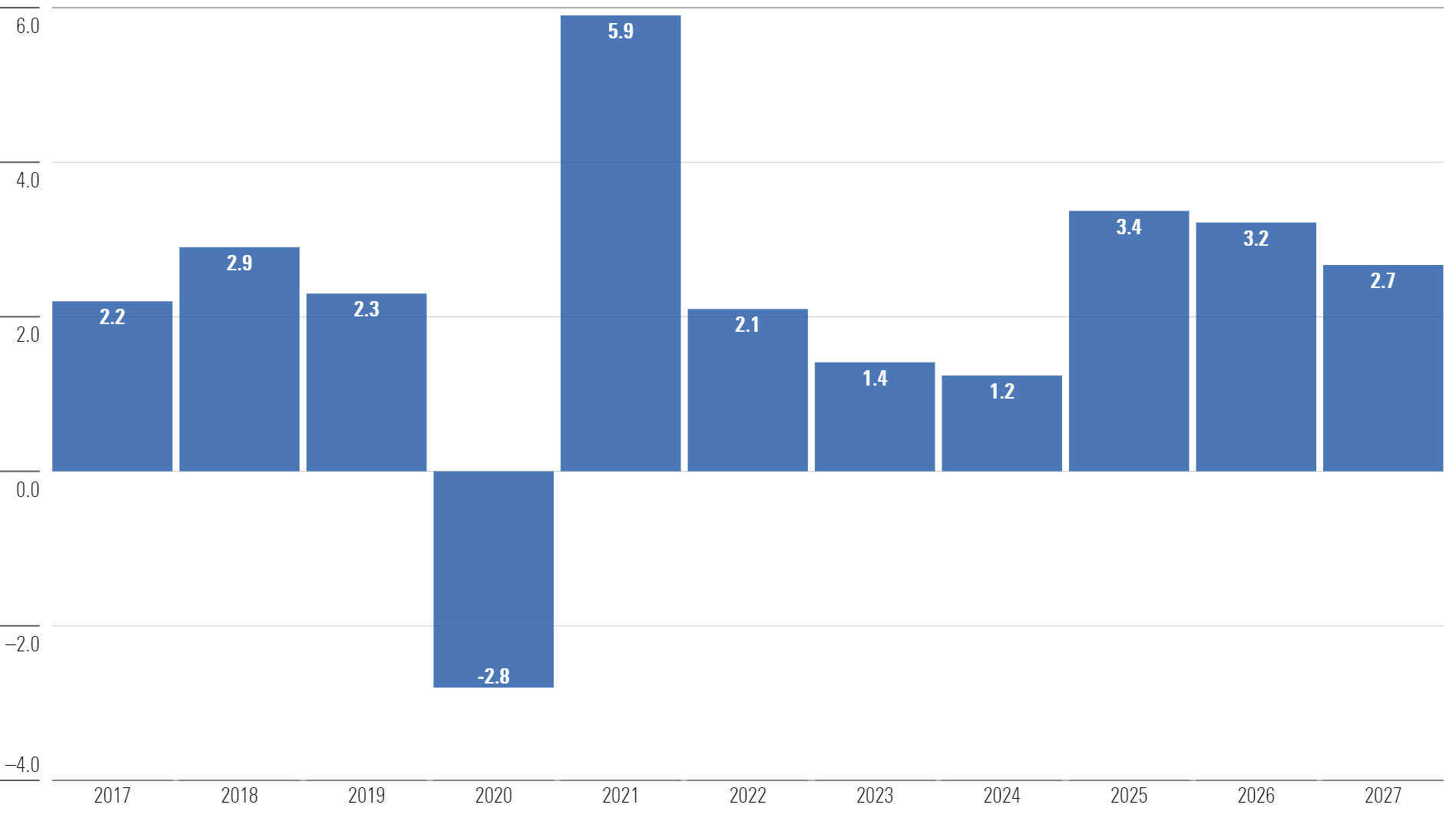

Fed Rate Cuts Will Jump-Start GDP Growth

We expect that GDP growth will start accelerating in second-half 2024 as the Fed pivots to easing, with full-year growth numbers peaking in 2025 and 2026. The resolution of supply constraints should facilitate an acceleration in growth without inflation becoming a concern again.

U.S. Real GDP Growth (%)

We expect a cumulative 4% to 5% more real GDP growth through 2027 than the consensus does. Consensus remains overly pessimistic on the recovery in the labor supply and has overreacted to near-term productivity headwinds, in our view.

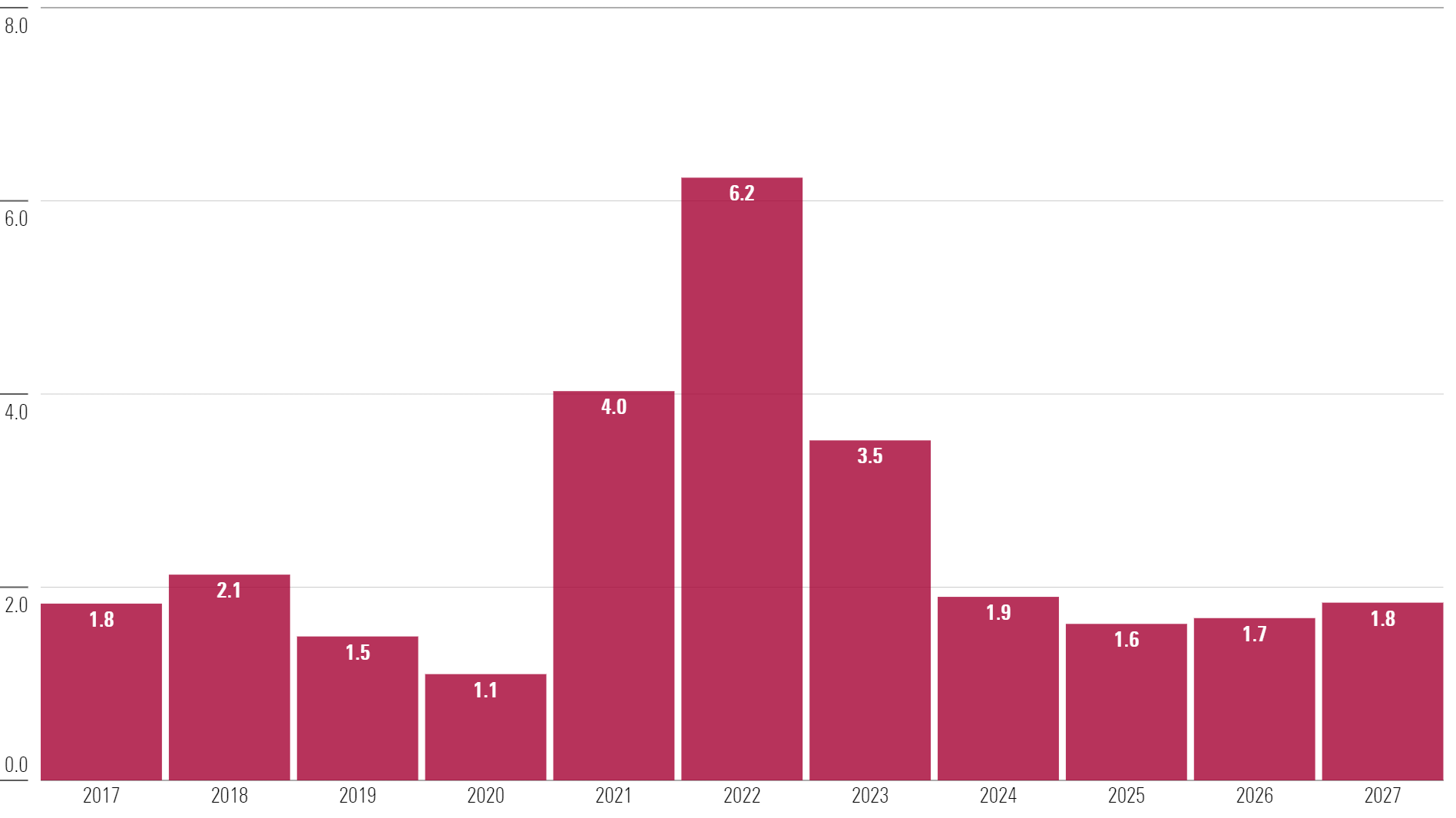

Resolution of Supply Constraints Plus Fed Tightening Will Crush Inflation

We expect inflation to fall to normal levels after peaking at 6.2% in 2022. We still think most of the sources of high inflation since the start of the pandemic will abate (and even unwind in impact) over the next few years. This includes energy, autos, and other durables. Aggressive capacity expansion across many areas could turn widespread shortages into gluts within a few years. Combining these factors with monetary policy tightening, we expect inflation to drop to 3.5% for full-year 2023 and average just 1.8% over 2024-27.

U.S. Inflation Rate (PCE Index, %)

We’re more optimistic on inflation coming down than consensus. We think consensus underrates the deflationary impulse likely to be provided by industries like energy and durable goods in coming years, as pandemic-era disruptions fade.

U.S. Interest-Rate Forecast: What We See for the Future

In the short run, our interest-rate forecast is centered on the Fed and its attempt to smooth out economic cycles. The Fed seeks to minimize the output gap (the deviation of GDP with its maximum sustainable level) while keeping inflation low and stable. When the economy is overheated (the output gap is positive and inflation is high), as today, then the Fed seeks to hike interest rates to slow growth.

In the long run, the Fed largely disappears from the picture. Instead, interest rates are determined by underlying currents in the economy, like aging demographics, slower productivity growth, and higher economic inequality. These forces have acted to push down interest rates in the United States and other major economies for decades, by creating an excess of savings over investment. In other words, the natural rate of interest has shifted downward. These long-term drivers of low interest rates haven’t gone away and will return to the fore once the dust settles from the pandemic.

For this reason, our interest-rate forecast includes the expectation that these rates will stay lower for longer. Even if we’re wrong in our near-term view that the Fed’s war against inflation will be a short one, our long-term view on interest rates remains valid. Our long-term analysis was detailed in our 2022 U.S. Interest Rate & Inflation Forecast.

A version of this article was published on April 23, 2023.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/GJMQNPFPOFHUHHT3UABTAMBTZM.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/UYSRGR6ZLJFWXDECADZPSR7BJU.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MLKHO4HEDJETLPBTREPIAMGQBE.png)