Is Palantir Stock a Buy, a Sell, or Fairly Valued After Earnings and a Big Rally?

Palantir’s renewed interest in artificial intelligence keeps investors optimistic for continued growth.

Palantir PLTR released its first-quarter earnings report on May 8, 2023. Here’s Morningstar’s take on Palantir’s earnings and stock.

Palantir Stock at a Glance

- Fair Value Estimate: $9

- Morningstar Rating: 2 stars

- Morningstar Economic Moat Rating: Narrow

- Morningstar Uncertainty Rating: Very High

What We Thought of Palantir’s Earnings

- Earnings were slightly above our estimates, but the outperformance was offset by the fact that the firm’s annual outlook was largely similar to what it had provided previously. We see this as perhaps a case of pull-forward demand. To provide some context, Palantir’s most recent quarter was a $20 million beat of expectations, but the firm’s guidance for the full year was revised upward only $5 million.

- If you’re bullish on Palantir and its artificial intelligence opportunity, the earnings provide plenty of reasons to be optimistic. CEO Alex Karp had sound bites like: “We will take the entire market” (about AI). For other investors, and from our perspective, it is a show-me story. We are waiting for an acceleration in billings, remaining performance obligations, and deferred revenue—the typical forward-looking indicators for tech firms—which will indicate significant client interest in Palantir’s AI offerings.

We do think the market’s optimism is overdone. There are a few reasons:

- Palantir does AI, it always has. While there is an uptick in interest in AI (especially following ChatGPT and other GenAI-related product releases), it remains to be seen how this interest translates into companies and governments leveraging Palantir’s tools more.

- Macro turbulence continues to be a headwind for stock, leading investors to flee from high-growth tech to other sectors. Even as investors have returned, valuations have not returned to any semblance of what they were in 2021, even allowing for the bubble conditions of that year that led to tech firms trading at an enterprise value/next twelve months, or EV/NTM, of 40. But at the same time, investors remain concerned about the impact of a recession on customers’ buying behavior, especially as it pertains to IT spending.

- The median growth estimate for fiscal 2024 sales is 16%, well below other high-flying peers that are valued at 10-plus EV/NTM sales. To buy Palantir at these prices, investors must believe that this growth will both meaningfully accelerate and persist for far longer than previously thought.

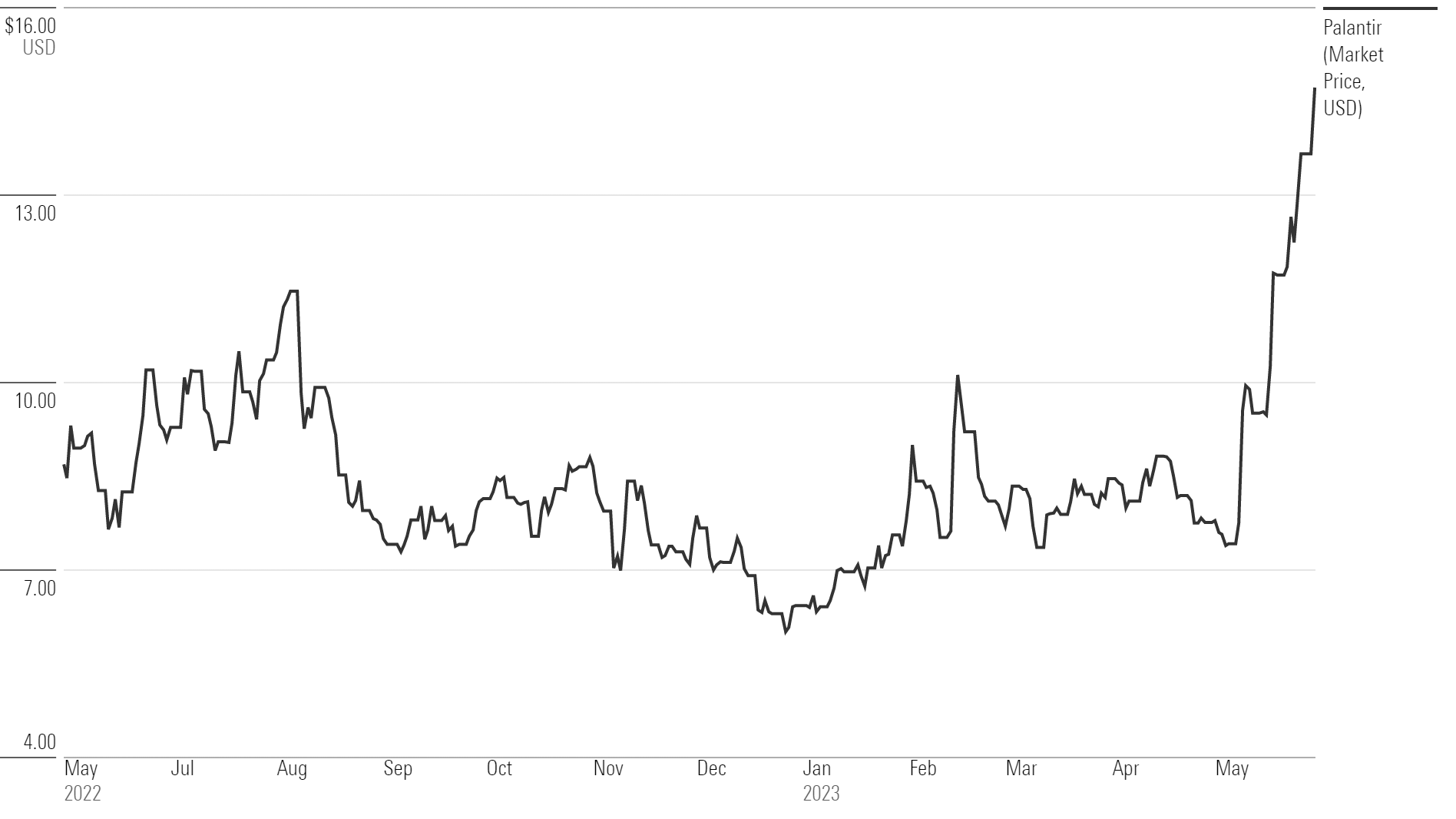

Palantir Stock Price

Fair Value Estimate for Palantir Stock

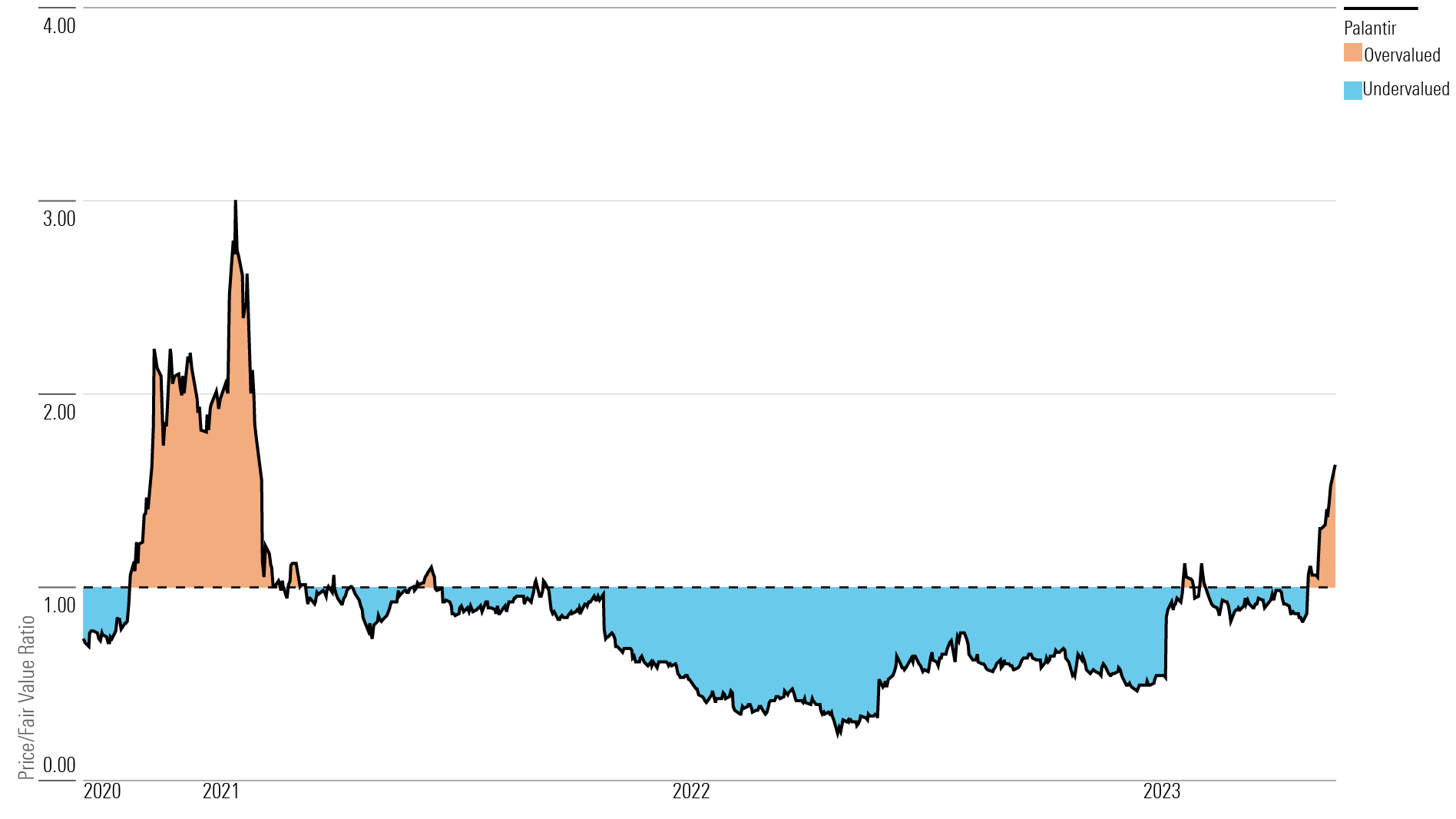

Our fair value estimate for Palantir is $9 per share, implying a 2023 enterprise value/sales multiple of 8 times. At a 2-star rating, Palantir stock is overvalued compared with its fair value estimate.

We forecast Palantir’s revenue increasing at a 22.5% compound annual growth rate over the next five years as the firm expands government and commercial operations. We expect the majority of this top-line growth to be driven by commercial clients as the firm seeks to broaden that client base. While government clients can be sticky, large government contracts create lumpiness in revenue. As a result, Palantir’s shift to more commercial clients will enable the firm to create a more ratable revenue mix.

We also expect the firm to continue expanding sales within its existing client base. We view Palantir’s strong net retention rate as an indicator of this ability.

Read more about Palantir’s fair value estimate.

Palantir Price/Fair Value Ratio

Economic Moat Rating

We assign Palantir a narrow economic moat rating owing primarily to strong switching costs associated with its platforms and also to intangible assets in the form of strong customer relationships the firm has built over the years. We think that Palantir’s two main platforms, Gotham and Foundry, both benefit from high customer switching costs as evidenced by the firm’s strong gross and net retention metrics. Palantir has exhibited strong customer growth while diversifying its business away from lumpy governmental contracts toward commercial clients. As a result, although we forecast a couple of more years of hefty operating losses, we ultimately expect the firm to generate excess returns over invested capital over the next decade.

Read more about Palantir’s moat rating.

Risk and Uncertainty

We assign Palantir a Very High Uncertainty Rating because of some key risks that we view as potentially impeding the firm’s growth trajectory.

While Palantir has landed high-value commercial and government clients over the years, we have found the executive team’s execution to be questionable at best. The firm’s sales strategy has led to relatively poor customer acquisition, despite being in the commercial space for many years, Palantir’s commercial customer count is only slightly more than 200. While the firm has pivoted to a module-based sales model that should bolster commercial customer additions, execution against this strategy remains to be seen.

Read more about Palantir’s risk and uncertainty.

PLTR Stock Bulls Say

- Palantir has strong secular tailwinds behind its back as the artificial intelligence/machine learning market is expected to expand rapidly because of the exponential increase in data harvested by organizations.

- With products targeting both commercial and government clients, Palantir has a distributed top line with the noncyclical governmental revenue insulating the firm’s top line during lean times.

- Palantir’s focus on modular sales could potentially lead to substantially more commercial clients, which the firm could subsequently upsell.

PLTR Stock Bears Say

- By not selling to countries/companies that are antithetical to Palantir’s mission and cultural values, the firm has self-restricted its growth opportunities.

- It will likely be several years before Palantir will achieve GAAP profitability.

- Palantir’s executive team has made questionable strategic decisions in the past. While past performance isn’t necessarily indicative of future results, we highlight some missteps as a tale of caution for potential investors.

This article was compiled by Maggie Guidici.

Get access to full Morningstar stock analyst reports, along with data and tools to manage your portfolio, through Morningstar Investor. Learn more and start a seven-day free trial today.

The author or authors do not own shares in any securities mentioned in this article. Find out about Morningstar’s editorial policies.

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/MG6XOCYGF5BO7MG5YRNBISB3SA.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/TXAOQ3NTDNAVLGMP3O4BVUVFTA.png)

:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/RH6K4NMACRHO3DQIPX57HVLLAU.png)